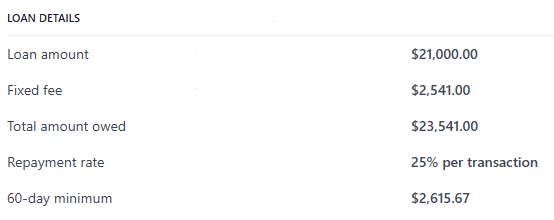

This is a real offer someone sent me that their client is getting offered from Stripe Capital. Even though its a loan by their legal categorization, it works just like an MCA. If you do the math it's basically a 1.121

Your thoughts?

This is a real offer someone sent me that their client is getting offered from Stripe Capital. Even though its a loan by their legal categorization, it works just like an MCA. If you do the math it's basically a 1.121

Your thoughts?

After pondering my thoughts and 2cents worth, others that worked for Kapitus or Fora in the past would carry more weight with their comments than myself because they are or were (in-house) Just possibly, Stripe may have a controlled business arrangement with very specific "A" rate buy rates for a 1.121 FR. That buy rate Stripe receives could also be the sell rate with a very small layer of profit, but if the volume dictates as I'm sure it does, Stripe makes origination fees or collects a fee in addition to performance fees as the MCA seasons with timely payments from that client. Then again, Stripe is so large and voluminous with MCA funding volume, that they risk manage in-house all credit grade MCA's. Sure with all the talent in our marketplace, the correct answer will appear. Also, hat off to Shane as one of the sharpest in our industry with business and pure commonsense creativity. Heard all good things about Shane.

If it's true, they self finance it. Kapitus or anyone else can't really make any profit @1.121 FR. Without lots of fees for offset. Can't blame Stripe as they have the gold and captive merchant. Everyone and their mother is in our business and Stripe has the client. Can't compete with that FR. Shane's covert spidy senses must kick in to find out a credit score for this merchant. Could be a "reel me in" come on and then FR changes after Stripe pulls their credit report or goes from their initial credit report when they approved the merchant for processing. Just maybe and I'm sarcastically spit balling here, but it's true, any questions the merchant has via telephone could be transferred to a third world country to keep costs low and the client could get frustrated. In the alternative David below or Us Trust Business Loans can snake the client and bring them to a comfortable realty. We will educate them about low rate LOC's if they are worthy and how a lower A.P.R. on a term loan will make their sinister MCA predatory. It all depends what side of the fence you/they are on....That's a wrap for my honest 2cents.

That's actually kindof insane

Woah.... Do you know their requirements for approval for deals like that?